Calculating pain and suffering car accident: A Practical Guide to Damages

Learn how calculating pain and suffering car accident damages works, with factors and tips to maximize your settlement.

After a car accident, figuring out compensation isn't just about adding up medical bills and car repair receipts. You also have to calculate the human cost of the crash—the pain, the stress, the way it's turned your life upside down. This is what's known in the legal world as "pain and suffering," and it's a critical part of any claim.

But how do you put a price on that? It’s not like there's an invoice for anxiety or a receipt for the sleepless nights. Instead, attorneys and insurance adjusters use a couple of standard methods, like the multiplier or per diem approach, to translate your experience into a dollar amount.

What “Pain and Suffering” Really Means in a Claim

When you file a personal injury claim, the money you're asking for falls into two buckets. The first is easy to understand; the second, not so much.

Let's quickly create a table to see how these two types of damages compare.

Economic vs Non-Economic Damages at a Glance

| Type of Damage | What It Covers | Example |

|---|---|---|

| Economic | Tangible, verifiable financial losses. | Medical bills, lost income, vehicle repair costs, pharmacy receipts. |

| Non-Economic | Intangible, subjective, and non-financial hardships. | Physical pain, emotional distress, loss of enjoyment of life, anxiety. |

As you can see, economic damages are the black-and-white costs. Non-economic damages—or pain and suffering—are the gray area.

This is the legal system's way of acknowledging the real, but hard-to-quantify, impact of an accident. It’s shorthand for the physical and emotional trauma you've been forced to endure.

Think of it as compensation for things like:

- Physical Pain: The chronic backache that won't go away, the splitting headaches, or the constant ache from a broken bone as it heals.

- Emotional Distress: This is the psychological fallout. It could be the panic you feel getting behind the wheel, the depression that's settled in, or even full-blown PTSD.

- Loss of Enjoyment of Life: Maybe you can't play catch with your kids anymore, tend to your garden, or go for your morning run. It’s for the hobbies and joys the accident stole from you.

Because this is all so subjective, calculating it is one of the most contentious parts of any settlement negotiation. An insurance company can’t just look up a price for your grief. So, they fall back on formulas to try and make it objective. The two big ones are the multiplier method and the per-diem approach, which we’ll dive into next.

This isn't a niche issue, either. Car accidents make up more than 50% of all personal injury cases in the United States, meaning this calculation happens thousands of times every single day. While no formula can perfectly capture your unique experience, understanding how they work is the first step toward figuring out what your claim might be worth. If you're curious, you can explore more data on how accident claims are valued in the U.S. to see how these numbers shake out in the real world.

A Real-World Look at the Multiplier Method

When an insurance adjuster starts crunching numbers for your pain and suffering, they almost always pull out their go-to tool: the multiplier method. It’s the industry-standard way to put a dollar figure on something as personal as your pain.

The concept itself is simple. They take your total "economic damages"—all the clear, billable costs—and multiply them by a number, usually somewhere between 1.5 and 5.

The formula looks like this: Economic Damages x Multiplier = Pain and Suffering Value.

But don't let that simple math fool you. The entire negotiation hinges on one thing: the multiplier. That single number is where the story of your accident, your injuries, and your recovery gets told. A 1.5 might be used for a minor fender-bender with a few weeks of chiropractor visits. A 4 or 5? That's reserved for life-changing injuries involving surgery, permanent impairment, or significant emotional trauma.

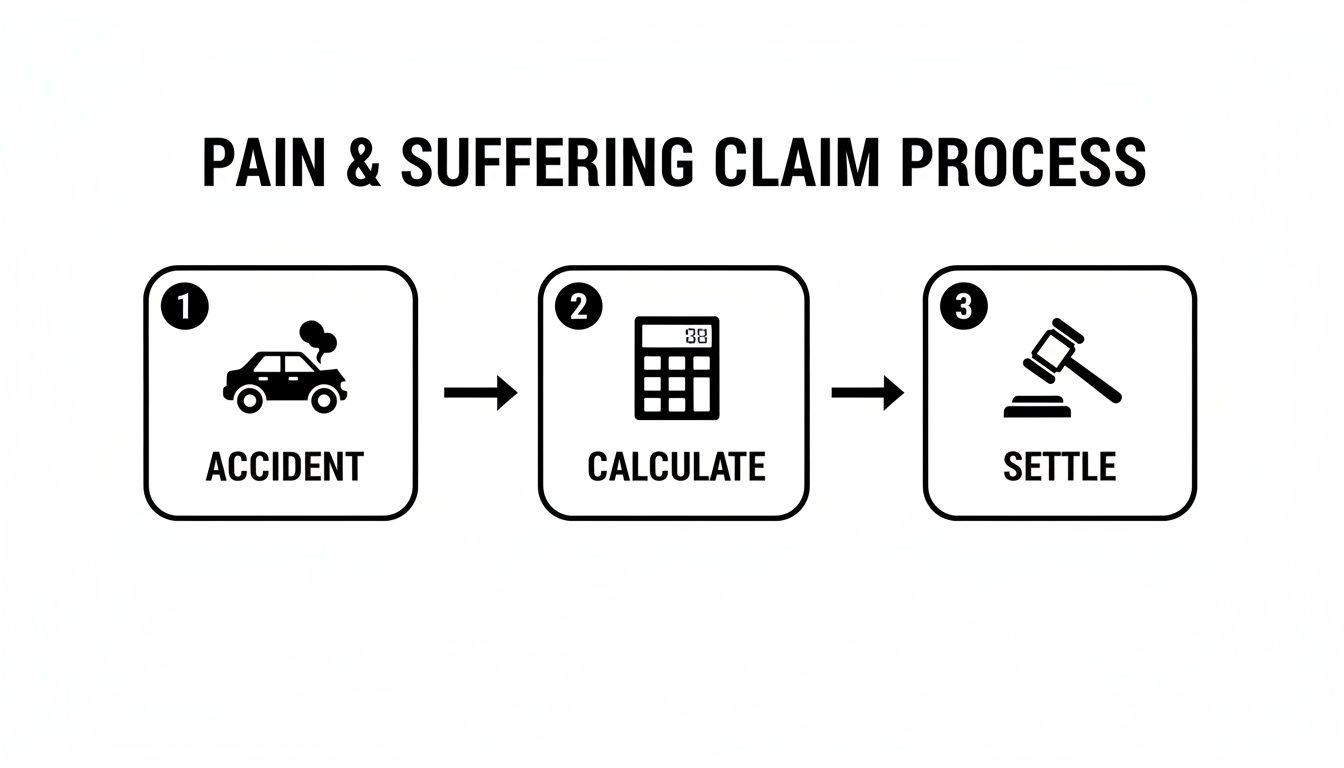

The whole process really boils down to three phases: the crash happens, the damages get calculated, and then you work toward a settlement.

As you can see, that calculation step is the critical bridge connecting what you lost to what you can recover.

What Justifies a Higher Multiplier?

So, how do you argue for a 3 instead of a 1.5? It's all about building a compelling case backed by solid proof. Adjusters and attorneys look for specific factors that clearly show how significantly the accident impacted your life.

Here are the heavy hitters that tend to push the multiplier up:

- Severity and Permanence of the Injury: A fractured femur that requires surgery is a world away from a soft tissue sprain. Chronic pain or a permanent limp will always command a higher multiplier.

- The Need for Invasive Treatment: If your recovery plan included surgery, steroid injections, or other serious medical interventions, the multiplier goes up. These procedures inherently involve more pain and risk.

- How Long Recovery Takes: A recovery that drags on for months—or years—is a clear indicator of prolonged suffering. The longer you're dealing with it, the higher the multiplier should be.

- Visible Scarring or Disfigurement: Permanent physical reminders of the accident carry immense emotional weight. This is a powerful factor that adjusters take very seriously.

- Diagnosed Psychological Trauma: If you have a documented diagnosis for PTSD, anxiety, or depression from a qualified professional linking it to the crash, it absolutely strengthens your claim for more compensation.

The multiplier isn't just a random number. It’s a reflection of the total disruption this accident caused in your life. The stronger your documentation, the more leverage you have to push for a number that truly reflects your experience.

Example: A Rear-End Collision in Dallas

Let's walk through a realistic scenario to see how this plays out. Imagine Sarah is stuck in traffic on the LBJ Freeway when she’s rear-ended. The jolt is severe, and she’s later diagnosed with a herniated disc in her lower back.

First things first, we have to add up all of her economic damages—the hard costs.

- Medical Expenses: $22,000 (This covers her ER visit, an MRI, specialists, and physical therapy.)

- Lost Income: $3,000 (She had to miss work for appointments and recovery.)

- Total Economic Damages: $25,000

Now for the pivotal part: choosing the multiplier. Sarah's injury is serious and has a major impact on her quality of life; she's in constant pain and had to give up her weekend hiking passion. While she doesn't need surgery right now, her doctor says it might be necessary down the road.

Her injury is much more severe than a simple sprain (which might get a 1.5 or 2), but it’s not catastrophic. A multiplier of 3 is a solid, defensible choice here.

Let's do the math:

- Economic Damages: $25,000

- Multiplier: 3

- Pain and Suffering Value: $25,000 x 3 = $75,000

To get her total initial demand, we add her economic damages and her pain and suffering value together: $25,000 + $75,000 = $100,000. This figure becomes the well-reasoned starting point for her negotiations with the insurance company.

A Different Approach: Using the Per Diem Method to Value Your Recovery

While the multiplier is a go-to tool, it’s not the only way to tackle the problem of calculating pain and suffering from a car accident. There's another approach called the per diem method, which can be incredibly effective for injuries with a clear, finite recovery timeline. "Per diem" is just Latin for "per day."

Instead of using a multiplier, this method assigns a specific dollar amount to every single day you were in pain because of the accident. The clock starts ticking the moment the crash happens and only stops when your doctor confirms you’ve reached “maximum medical improvement” (MMI). MMI is the point where your condition is stable and isn't expected to get any better. It's a very logical, day-by-day accounting of your ordeal.

How Do You Pinpoint a Fair Daily Rate?

The entire per diem method hinges on setting a daily rate that makes sense. You can't just pick a number out of the blue; it needs to be backed by a solid argument that an insurance adjuster—or a jury—will find reasonable.

The most common and persuasive way to do this is to anchor your daily rate to your daily earnings.

The logic here is simple and powerful. You can argue that if a day of your labor is worth a certain amount, then a day spent enduring pain, frustration, and physical limitations is worth at least that much. You're effectively making the case that managing the aftermath of a serious injury is just as demanding as your job, if not more so.

To calculate your daily rate, you simply take your gross annual salary and divide it by the number of working days in a year, which is generally accepted to be around 250. So, if you earn $60,000 a year, your suggested daily rate would be $240 ($60,000 / 250). This gives you a concrete, defensible figure to start negotiations with.

Let's Walk Through a Real-World Per Diem Calculation

Let's see how this plays out in a practical scenario. Imagine Mike, an electrician from Fort Worth earning $52,000 a year, gets T-boned and suffers a broken clavicle and severe bruising.

First things first, we need his daily rate.

- Annual Salary: $52,000

- Daily Rate: $52,000 / 250 workdays = $208 per day

Next, we look at his recovery time. Mike’s doctors carefully documented his entire journey, from the ER to physical therapy sessions. After 150 days, his primary physician officially declared he had reached maximum medical improvement. That 150-day window is the duration we use.

Now, we can put it all together to get his total pain and suffering value:

- Daily Rate: $208

- Total Recovery Days: 150

- Total Per Diem Value: $208 x 150 = $31,200

This $31,200 is the value of Mike’s non-economic damages. When his attorney sends a demand to the insurance company, the total settlement amount would be this figure plus all his economic damages (like medical bills and lost income).

Key Takeaway: The beauty of the per diem method is its straightforward logic. It takes something as abstract as daily suffering and translates it into a tangible dollar amount tied directly to your earning power, which makes for a very compelling argument.

When Does the Per Diem Method Work Best?

The multiplier and per diem methods aren't always interchangeable. Each has situations where it shines.

The per diem approach is often most effective for:

- Injuries with a Clear Finish Line: Things like broken bones, post-surgery recovery, or soft tissue injuries that eventually heal completely. When a doctor can definitively say, "Your recovery took X days," the math is clean and easy to justify.

- Cases with Low Medical Bills but a Long Recovery: If your medical expenses were relatively small but you were laid up in pain for months, the multiplier method might give you a pretty low number. The per diem method does a much better job of capturing the duration of your suffering.

On the other hand, this method falls short for catastrophic or permanent injuries. For someone dealing with chronic pain, a lifelong disability, or permanent disfigurement, the suffering doesn't just stop. In those tragic cases, the multiplier method is almost always the better choice to account for a lifetime of future pain and suffering.

What Actually Drives Your Claim's Value Up or Down?

The multiplier and per diem methods are great starting points for putting a number on pain and suffering, but they’re just that—a start. The final value of your claim isn't some abstract calculation. It's a figure hammered out in the real world, shaped by a handful of key factors that can either make your case compelling or give the insurance company an easy way out.

Think of it this way: adjusters (and juries, if it comes to that) are looking at the whole picture to decide what your suffering is truly worth. Knowing what they’re looking for is the difference between taking a lowball offer and negotiating from a position of real strength. Your economic damages—the medical bills and lost wages—are the foundation. These other factors are what determine how tall the final building stands.

Key Factors That Strengthen Your Claim

Some details just scream "serious injury" to an insurance company. When they see these elements, they know they can't just dismiss your claim. These are the facts that paint a clear, undeniable picture of what you've been through since the accident.

- Objective, Verifiable Injuries: All pain is real, but injuries you can see on an X-ray, MRI, or CT scan are much harder for an adjuster to argue with. A fractured vertebra or a torn ligament is concrete proof that something serious happened.

- Consistent Medical Treatment: If you were hurt, you’d see a doctor, right? That’s how adjusters think. Getting medical help right away and sticking to your doctor's recommended treatment plan shows you’re serious about getting better and that your injuries are legitimate. Gaps in treatment are a red flag they love to wave.

- Referrals to Specialists: When your family doctor sends you to an orthopedist, neurologist, or pain management specialist, it’s a powerful endorsement. It signals that your injuries are complex and severe enough to require an expert's care.

- Permanent or Long-Term Impact: This is a huge one. Will you have a permanent limp? A visible scar? Chronic pain that will never fully go away? Any lasting consequence dramatically increases the value of your claim because it represents a lifetime of dealing with the fallout of the accident.

The type of injury and its long-term effects are central to the final number. A minor whiplash case might resolve for a modest amount, but a moderate herniated disc that requires months of physical therapy can easily push a settlement into the $20,000–$100,000 range. For catastrophic injuries that require surgery or result in paralysis, the value often soars past $100,000, sometimes into the millions. This shows why every piece of evidence matters.

Factors That Can Weaken Your Claim Value

Just as some facts build your case up, others can give an insurance adjuster the ammunition they need to tear it down. Their job is to protect their company's bottom line, so they are actively looking for reasons to pay you less.

Here are some of the most common issues that can hurt your claim:

- Pre-existing Conditions: If you had a bad back before the accident, you can bet the insurer will argue the crash just aggravated an old problem, rather than causing a new one.

- Gaps in Treatment: Skipping appointments or waiting weeks to see a doctor can be spun as proof that you weren't really in that much pain.

- Inconsistent Statements: Contradictions are a killer. If you tell your doctor one thing, say something different in a recorded statement, and post pictures of yourself hiking on social media, your credibility is shot.

- Shared Fault in Texas: This is a big one here. Texas operates under a "modified comparative fault" rule. If you're found to be partly at fault for the crash, your final award is reduced by that percentage. But if you're found 51% or more at fault, you get absolutely nothing.

The table below breaks down how these different factors can influence the multiplier used in your pain and suffering calculation.

Factors Influencing Your Pain and Suffering Multiplier

| Factor | Impact on Multiplier | Example Scenario |

|---|---|---|

| Clear, objective injuries | Increases | An MRI clearly shows two herniated discs in your neck. |

| Delayed medical treatment | Decreases | You waited three weeks after the accident to see a doctor. |

| Referral to multiple specialists | Increases | Your PCP referred you to an orthopedist, who then sent you to a neurologist. |

| Pre-existing condition | Decreases | You had documented back pain from an old sports injury before the crash. |

| Permanent impairment/scarring | Significantly Increases | The accident left you with a permanent limp and a noticeable scar on your face. |

| Inconsistent statements | Significantly Decreases | You told the adjuster you couldn't work but posted vacation photos online. |

As you can see, the specifics of your situation matter immensely. An adjuster will weigh all these points to decide where on the scale your claim falls.

The single most powerful tool you have is documentation. A detailed journal tracking your daily pain levels, emotional state, and physical limitations can be incredibly persuasive. It transforms your claim from a set of medical bills into a human story of struggle and resilience.

Ultimately, your goal is to build a case so solid that there’s no room for the adjuster to downplay what you’ve endured. Every medical record, photo, and prescription receipt helps build the narrative that justifies the compensation you're seeking.

If you want to dive deeper into the nuts and bolts of the entire process, check out our comprehensive guide on how car accident settlements are calculated for more detailed insights.

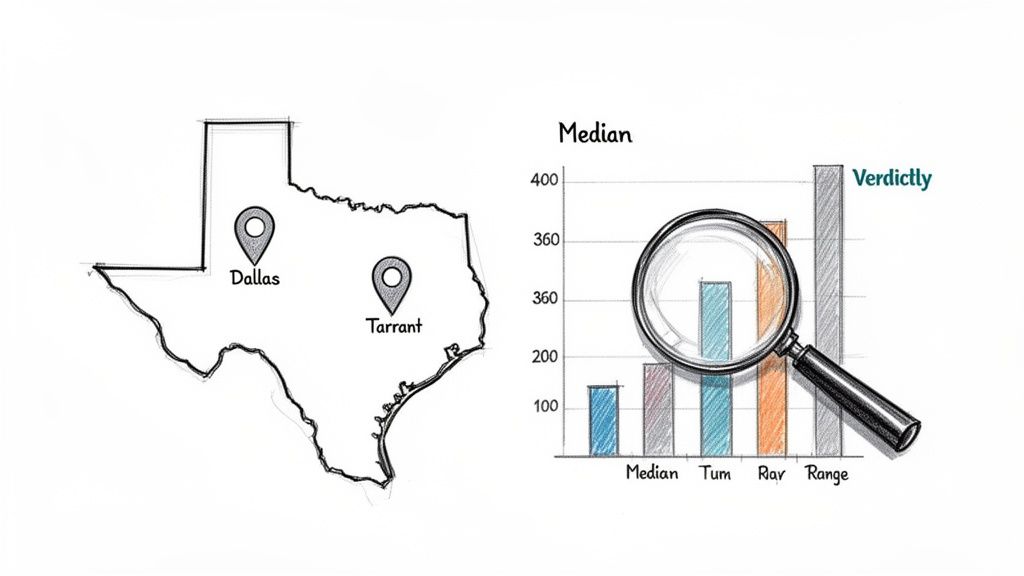

Using Real Texas Case Data to Benchmark Your Claim

The multiplier and per diem methods are great starting points. They give you a number to work with. But a number calculated in isolation doesn't mean much until you see how it stacks up against what's really happening in Texas courtrooms. This is where the real work begins—transforming your estimate from a guess into a data-backed negotiating tool.

Here’s the problem with generic online calculators: they don't know the difference between Harris County and Tarrant County. And believe me, there's a difference. What a jury in Austin might award for a herniated disc can be a world away from a similar case in Dallas. Relying on national averages is like trying to navigate Houston with a map of Chicago. It's not going to end well.

That’s why you have to ground your expectations in local case outcomes. Instead of just picking a multiplier out of thin air, you can see what’s been implicitly accepted in past settlements for injuries just like yours. You're moving from theory to reality, which puts you in a much stronger position at the negotiating table.

Tapping into a Database of Texas Verdicts

So, how do you find this information? The key is getting access to comparable case results. Platforms like Verdictly do the heavy lifting by compiling publicly available court records and settlement data into a searchable database. This is how you stop guessing and start analyzing what claims like yours are actually worth in your specific part of Texas.

With this kind of data, you can have a much more productive conversation with your attorney. Together, you can build a strategy based not just on legal principles, but on concrete examples of what has actually worked before.

Filtering for Cases That Mirror Yours

To get a useful benchmark, you need to compare apples to apples. A good database lets you drill down and find cases that are almost identical to your own situation.

You should be able to filter your search by the details that matter most:

- Injury Type: This is non-negotiable. A traumatic brain injury case has nothing in common with a soft tissue sprain claim. You need to isolate cases with the same, or very similar, diagnoses.

- Accident Location: It's crucial to filter by the specific Texas county where the crash happened. Jury pools, local precedents, and even judicial tendencies can vary dramatically from one place to the next.

- Collision Details: The mechanics of the crash matter. Were you rear-ended? T-boned? Was it a multi-car pileup? These details can influence everything from liability arguments to final settlement values.

By layering these filters, you create a hand-picked list of cases that serves as a powerful reality check for your own claim. This data-first approach to calculating pain and suffering car accident damages is how modern, effective claims are built.

By analyzing outcomes from your specific county and for your specific injury, you create a data-backed anchor for your settlement demand. This makes it much harder for an insurance adjuster to dismiss your numbers as arbitrary.

Analyzing the Data to Set Realistic Expectations

Once you have a solid list of comparable cases, it's time to dig in. Don't get distracted by one or two huge verdicts. Instead, look for the patterns and the typical range of outcomes.

Focus on these key data points:

- Median Award: The median is the true middle value—half the awards are higher, and half are lower. It's a much more reliable number than the average, which can be easily skewed by a few outlier cases.

- Settlement Range: What's the floor and what's the ceiling? Seeing the low, high, and median values gives you a realistic spectrum of what's possible.

- Case Summaries: This is where the context is. Read the details. What were the medical bills? Were there extenuating circumstances, like an incredibly sympathetic plaintiff or undeniable proof of the other driver's gross negligence?

Let's say you find that for herniated disc injuries in Tarrant County from rear-end collisions, the median award is $85,000. You also see a common settlement range between $40,000 and $150,000. Armed with that specific data, you and your attorney can confidently push back when an adjuster makes a lowball offer of $25,000, showing them it's completely out of line with the established norm. To see how these numbers fit into the bigger picture, our overview of a compensation calculator for car accident claims offers additional insight.

This data-driven strategy takes the emotion and guesswork out of the equation. It arms you with the same kind of information insurance companies use to value claims, which levels the playing field and ensures you're negotiating from a position of strength.

Common Questions About Pain and Suffering Claims

Even after you get a handle on the multiplier and per-diem methods, a lot of questions usually pop up. That’s perfectly normal. Calculating pain and suffering after a car accident is full of nuances and potential traps, especially here in Texas. Let's walk through some of the most common things people ask so you can move forward with more confidence.

Understanding these details can be the difference between getting a fair settlement and getting stuck in a frustrating, drawn-out fight with an insurance company. Knowing the answers is your best defense.

Can I Calculate Pain and Suffering Myself Without a Lawyer?

You can absolutely use the methods we’ve talked about to get a ballpark figure, but handling this on your own is a huge risk. Insurance adjusters are trained professionals whose entire job is to pay out as little as possible on your claim. They see hundreds of these cases and know every trick in the book to devalue your settlement.

Bringing in an experienced personal injury attorney changes the game completely.

- They live and breathe the complexities of Texas personal injury law.

- They know how to package your evidence for maximum impact.

- They can use real-world case data from platforms like Verdictly to shut down lowball offers.

Honestly, a good lawyer often finds value in a claim that you might never have known existed. Just having them on your side signals to the insurer that you're serious and won't be pushed around.

How Does the Texas Comparative Fault Rule Affect My Claim?

This is probably one of the most critical legal hurdles for any car accident victim in Texas. Our state follows a 51% "modified comparative fault" rule, which can make or break your ability to recover anything at all.

Here’s a simple breakdown of how it works:

- If you are found to be 51% or more at fault for the accident, you are legally barred from recovering a single penny.

- If your fault is 50% or less, your final compensation is just reduced by whatever your percentage of blame is.

Let's look at an example. Say a jury agrees your total damages are $100,000, but they also decide you were 20% at fault. Under Texas law, your $100,000 award gets cut by that 20%, so you would walk away with $80,000. This rule is exactly why proving the other driver was overwhelmingly responsible is a top priority in every claim.

What Is the Most Important Evidence for My Claim?

There’s no magic piece of evidence that guarantees a big settlement. The real strength of a claim comes from weaving together a collection of consistent and compelling documents that tell the undeniable story of what you've been through.

The most powerful claims are built on a foundation of diverse and consistent proof. Each piece of evidence supports the others, creating a comprehensive picture of the accident's true impact on your life.

Think of it like building a case brick by brick. Some of the most crucial pieces you'll need are:

- Detailed Medical Records: These are non-negotiable. They must clearly link your injuries directly to the car accident.

- A Personal Journal: This is your story, in your own words. Keep track of your daily pain, emotional struggles, sleepless nights, and all the things you can no longer do.

- Photos and Videos: Visuals are incredibly impactful. Snap clear photos of your injuries as they heal, the vehicle damage, and the accident scene.

- Witness Testimony: Hearing from friends, family, or coworkers about how the accident has changed you can be incredibly persuasive to an adjuster or jury.

Together, these elements transform your claim from a dry list of expenses into a powerful human story. For a deeper dive into the proof you'll need, check out our guide on how to prove pain and suffering for a complete checklist.

At Verdictly, we believe that access to real case data empowers you to have a more informed and fair negotiation. Our platform makes it easy to see what cases like yours are actually worth in Texas, so you can move forward with confidence. Explore real Texas verdicts and settlements today.

Related Posts

Pain and Suffering Calculation (pain and suffering calculation): Texas Damages

Explore how the pain and suffering calculation works in Texas, including multiplier and per diem methods, to help you estimate your settlement.

What to Do After a Hit and Run Car Accident in Texas

A complete guide on what to do after a hit and run car accident in Texas. Learn the critical first steps, your legal options, and how to file a claim.

Kinds of Negligence (kinds of negligence): How They Impact Your Injury Claim

Discover kinds of negligence in Texas personal injury cases and how they can impact your motor vehicle claim. Get clear guidance on your rights now.