Navigating Texas Parking Lot Accident Law A Complete Guide

Feeling lost after a crash? Unpack Texas parking lot accident law, from proving fault to fighting for fair compensation. Your practical guide starts here.

It’s easy to write off a parking lot collision as just a minor fender bender. But when it comes to the law here in Texas, these "simple" accidents are surprisingly complex. The reality is that fault isn't always as simple as pointing a finger at one driver. In fact, everyone from distracted drivers to the property owners themselves can share legal responsibility for the crash.

Why Parking Lot Accidents Are So Deceptive

The speeds are low, so the danger seems minimal. That’s a common—and misleading—assumption. Parking lots are uniquely chaotic environments where the usual rules of the road often feel more like suggestions. Drivers are hunting for spots, checking their phones, and managing kids in the back, while pedestrians, including small children, can dart out from between cars without a moment's notice.

This creates a perfect storm for collisions. It's not a small problem, either. According to recent insurance industry data, a staggering 40% of all vehicle damage claims happen in parking lots. That statistic alone highlights the hidden risk in these low-speed zones. Across the U.S., we see over 100,000 reported parking lot accidents every year, and about 15% of those result in injuries serious enough to need medical care. You can dig deeper into these numbers with these parking lot accident statistics.

More Than Just a Driver's Mistake

There's a persistent myth that parking lot accidents are automatically a 50/50 split of fault. That’s simply not true under Texas law. Every case gets decided based on its own specific facts. Fault isn’t just about who hit whom; it's about determining who failed to act with reasonable care under the circumstances.

Think about a driver backing out of a parking space. They have a clear duty to make sure the coast is clear before they move. If they hit a car that's already driving down the lane, the backing driver is almost always going to be found at fault. But what if both drivers were backing out at the same time? In that scenario, the fault could very well be shared.

The Property Owner’s Role in an Accident

Sometimes, the responsibility extends far beyond the two drivers. Property owners have a legal obligation to keep their premises reasonably safe for people who come onto their property. This concept, known as premises liability, is a crucial factor in many parking lot accident claims. A property owner could be found partially, or even entirely, liable if unsafe conditions on their lot helped cause the crash.

Key Takeaway: Figuring out who's at fault in a parking lot accident means looking at the whole picture. It requires a close look at driver actions, the flow of traffic, and the physical condition of the parking lot itself.

What kind of unsafe conditions could make a property owner liable? Here are a few common examples:

- Poor Lighting: Dim or burned-out lights in a parking garage or lot can make it incredibly difficult for drivers and pedestrians to see one another.

- Confusing Layout: Faded lane markings, a lack of proper stop signs, or a poorly designed traffic pattern can breed confusion and lead directly to collisions.

- Hidden Hazards: Things like massive potholes, unmarked speed bumps, or overgrown bushes that block the view at an intersection can be direct causes of an accident.

When you're involved in a parking lot accident, understanding these factors is the first step toward protecting your rights. What seems like a simple fender bender on the surface can quickly turn into a complex legal puzzle over who is truly responsible for your damages.

To make this clearer, let's break down the potential parties who could be held legally responsible in a Texas parking lot accident.

Who Can Be Held Legally Responsible

| Liable Party | Common Reason for Liability | Legal Principle Involved |

|---|---|---|

| A Driver | Distracted driving, failing to yield, backing up unsafely, speeding. | Negligence |

| Property Owner | Poor lighting, potholes, confusing layout, lack of security. | Premises Liability |

| Third Party | A pedestrian darting into traffic, another driver's actions causing a chain reaction. | Comparative Fault |

| Vehicle Manufacturer | A defective part (e.g., brake failure) causing the collision. | Product Liability |

Each of these scenarios introduces a different legal angle, which is why it's so important not to make assumptions about who is at fault after a crash.

The Legal Rules That Govern Your Claim

To make sense of what happens after a parking lot crash, you first have to get a handle on the legal ideas that will shape your claim. It might sound complicated, but the core concepts are actually pretty straightforward. In Texas, most parking lot accidents boil down to one central idea: negligence.

Think of negligence as a basic test with four questions. To have a valid legal claim, you have to be able to answer "yes" to all four. If even one answer is "no," the whole claim falls apart.

The Four-Part Test for Negligence

At its heart, negligence simply means that someone didn't act with the reasonable care you'd expect from a sensible person, and their carelessness ended up hurting someone else. In a Texas parking lot accident, you have to prove these four things to show someone was negligent.

- Duty: First, did the other person owe you a legal "duty of care"? In a parking lot, the answer is almost always yes. Every single driver has a basic duty to operate their vehicle safely to avoid plowing into other people. This means yielding, driving at a safe speed, and actually looking where they're going.

- Breach: Next, you have to show that the person breached that duty. This is the specific thing they did wrong. Maybe they rolled through a stop sign, tried to text while backing out, or zipped through a feeder lane like it was a racetrack. All of these are clear breaches of a driver's duty.

- Causation: This is the link in the chain. You must prove that the other driver's careless action is what actually caused the accident and your injuries. Put simply, if they hadn't breached their duty, you wouldn't have gotten hurt.

- Damages: Finally, you have to show you suffered real, provable damages. This isn't just about feeling wronged; it's about measurable losses. We’re talking about things like medical bills, lost paychecks, and car repair costs, as well as the non-economic harm like your pain and suffering.

Imagine a driver staring at their phone, completely missing a pedestrian in a marked crosswalk. The driver hits the person, breaking their leg. It’s a textbook case: the driver had a duty to watch out, breached it by being distracted, caused the injury, and the pedestrian suffered clear damages. All four parts are there.

When the Property Owner is at Fault

Sometimes, the driver isn't the only one to blame. The owner of the parking lot also has a legal responsibility to keep their property reasonably safe for visitors. This is a concept known as premises liability.

So, when might a property owner be on the hook? They could be held liable if they knew about—or should have known about—a dangerous condition and did nothing to fix it.

Common examples include:

- Terrible Lighting: Murky, poorly lit garages where it’s impossible to see pedestrians or other cars until it’s too late.

- Dangerous Potholes: Giant cracks or craters that can cause a driver to swerve or a pedestrian to take a nasty fall.

- No Clear Signage: Faded or missing stop signs, yield signs, or crosswalk markings that create chaos and confusion.

- Negligent Security: A total lack of security measures like cameras or patrols, especially in lots with a history of crime.

These issues aren't just minor annoyances; they can directly cause an accident, making the property owner at least partially responsible. People tend to think of parking lots as low-speed, low-risk zones, but the reality is shocking. Data reveals that over 500 people die in U.S. parking lots and garages every single year, a grim statistic that highlights just how dangerous they can be.

The field of parking lot accident law tackles these risks by looking at both driver negligence and the property owner's responsibility, especially when hazards like poor lighting are involved. You can get a deeper understanding of these dangers by reviewing these parking lot accident statistics.

The Frustration of a Hit-and-Run

A hit-and-run in a parking lot is a uniquely awful experience. One minute you're putting away groceries, the next a driver slams into your car and speeds off, leaving you to clean up the mess. While tracking down the person responsible is tough, it's not always a lost cause.

Your First Move is Crucial: Call the police right away to file an official report. Then, immediately start asking nearby stores and businesses if their security cameras might have caught the incident. That footage could be the single most important piece of evidence you get.

If you hit a dead end and the driver is never found, your own insurance policy is your lifeline. This is precisely what your Uninsured/Underinsured Motorist (UM/UIM) coverage is for. It's designed to step in and help pay for your medical bills and other damages when the at-fault driver is a ghost.

How Shared Fault Affects Your Compensation

There's a common and costly myth that if you're even a tiny bit to blame for a parking lot accident, you can't collect a dime. That's simply not true. Texas law is actually much more reasonable, using a system that assigns responsibility proportionally.

This system is officially called modified comparative fault, but a much easier way to think of it is the “51% bar” rule. The law recognizes that accidents are messy and rarely 100% one person's fault. So, instead of completely denying your claim for having a small share of the blame, the court simply reduces your final compensation by your percentage of fault.

Understanding this is critical. Why? Because insurance adjusters often prey on the public's confusion about shared fault, using it as a powerful negotiation tactic to slash their payout.

Understanding The 51 Percent Bar Rule

The rule is surprisingly straightforward. You are eligible to recover damages as long as you are found to be 50% or less responsible for the accident. The moment your share of the blame hits 51% or more, you lose the right to recover anything from the other party.

Let's walk through a real-world example. Say you're driving down the main lane of a busy shopping center parking lot. A driver, distracted while hunting for a spot, suddenly pulls out from a parking aisle without looking and smacks into your rear passenger door. Your total damages, from medical bills to car repairs, add up to $20,000.

During the claim process, the other driver’s insurance company argues you were going a little too fast for a crowded lot. After some back-and-forth, it's determined that you were 10% at fault.

Here’s how the math plays out:

- Total Damages: $20,000

- Your Percentage of Fault: 10%

- Reduction Amount: $2,000 (which is 10% of $20,000)

- Your Final Compensation: $18,000

You still walk away with the vast majority of your damages because your fault fell well below that 51% cliff. Had you been found 60% at fault, your recovery would have been zero. For a deeper dive into this rule, check out our complete guide on comparative negligence in Texas.

Shared Fault In Common Parking Lot Scenarios

This rule is a central player in nearly every parking lot collision, precisely because the facts can be so murky. Insurance companies are experts at finding ways to shift at least some of the blame onto you to minimize what they have to pay.

Key Insight: Expect the insurance adjuster to try and pin a higher percentage of fault on you than is fair. Knowing the 51% rule gives you the power to push back against these lowball tactics and demand an assessment that reflects what actually happened.

Think about these classic parking lot collision scenarios where fault is almost always debated:

- Two Cars Backing Out at the Same Time: When two cars back out of opposite spaces and hit each other, fault is often split 50/50. However, if one driver can prove the other started moving second and had a better chance to see them, the percentages could shift.

- A Crash at an Unmarked Intersection: In lots without stop or yield signs, every driver has a duty to be cautious. An investigator will look at who had the right-of-way (the driver on the right, or the one in the main thoroughfare lane) and who failed to keep a proper lookout.

- A Driver Cuts Through Empty Parking Spaces: We’ve all seen it. A driver cuts diagonally across empty spots instead of using the proper lanes. While that driver is almost certainly primarily at fault for any collision, the other driver could be assigned a small percentage of blame if they weren't paying attention.

Getting a handle on these nuances is one of the best ways to protect the full value of your claim.

Building a Rock-Solid Evidence File

The moments after a parking lot crash are a blur of confusion and adrenaline. But what you do right then and there can make or break your entire claim. The good news is, the most powerful tool for building your case is probably already in your hand: your smartphone.

Think of yourself as a detective. Your immediate job is to capture the scene exactly as it is, before anything gets moved or forgotten.

Document the Scene Like a Pro

Don't just take one quick picture of the damage. You need to tell a complete visual story. Get photos and videos from every possible angle, capturing details that might seem small but could become crucial later on.

- Vehicle Damage: Get up close on the dents and scrapes on both cars, but also step back for wide shots showing how the vehicles ended up.

- The Big Picture: Pan out and document the entire area. Are the parking lines faded and confusing? Is a crucial stop sign blocked by an overgrown bush? Is the lighting in the garage dangerously low? These details can sometimes point the finger of blame toward the property owner.

- Tire Marks & Debris: Look for skid marks on the pavement or any broken plastic and glass from the collision. Snap photos of it all.

- License Plates: A clear, readable photo of the other driver's license plate is an absolute must.

This visual record is often the most powerful piece of evidence you'll have. It locks in the details of the scene and prevents the other driver from changing their story down the road.

Crucial Tip: Always try to get a police report, even for a minor accident on private property. Some departments might be reluctant to respond, but an official report provides a neutral, third-party summary of the incident that insurance companies take seriously.

Gather Key Information from Everyone

Next, you'll need to collect the essentials from the other driver. Politely get their name, phone number, address, and insurance information. The easiest way to do this without errors is to simply ask if you can take a quick photo of their driver's license and insurance card.

If there are any bystanders who saw the accident happen, their input can be gold. Ask for their name and contact info. A neutral witness who can back up your side of the story carries a lot of weight, especially when it's your word against the other driver's. For more complicated cases, understanding what is expert witness testimony can also be helpful, as specialists might be brought in to analyze the very evidence you're collecting now.

To help you stay organized in the moment, here’s a quick checklist of what to gather at the scene.

Your Post-Accident Evidence Checklist

| Evidence Type | Why It's Critical | Actionable Tip |

|---|---|---|

| Photos & Videos | Creates an undeniable visual record of damage, vehicle positions, and scene conditions. | Take more than you think you need from multiple angles—wide shots, close-ups, and everything in between. |

| Driver Information | Essential for identifying the other party and initiating an insurance claim. | Snap a picture of their driver's license and insurance card to avoid typos. |

| Witness Contact Info | Provides a neutral, third-party account to support your version of events. | Get their full name and phone number. A quick text to confirm the number is a smart move. |

| Police Report | A formal, unbiased document that adds significant credibility to your claim. | Call the non-emergency police line to request an officer, even if the crash seems minor. |

| Medical Records | Directly links your injuries to the accident, forming the foundation of any injury claim. | See a doctor immediately, even if you feel fine. Adrenaline can hide serious injuries. |

Following this checklist helps ensure you don't miss a single critical piece of information needed to protect your rights.

Seek Medical Attention Immediately

This is the one step you cannot skip, even if you feel perfectly fine. The adrenaline surging through your body after a crash is incredible at masking pain. Injuries like whiplash, concussions, or internal bruising might not show symptoms for hours or even days.

Getting checked out by a doctor right away accomplishes two vital things. First and most importantly, it's about your health and well-being.

Second, it creates a medical record that officially connects your injuries to the exact time and date of the accident. This documentation is the absolute foundation of a personal injury claim. If you wait a week to see a doctor, the insurance company will argue that something else could have caused your injuries in the meantime. That delay gives them the perfect excuse to deny your claim.

How To Calculate Your Claim's Potential Value

After the dust settles from a parking lot crash, the biggest question on anyone’s mind is usually, "So, what's my case actually worth?" It's a fair question, and the answer isn't just pulled out of thin air. To figure out the potential value of your claim, you have to look at every single way the accident has turned your life upside down.

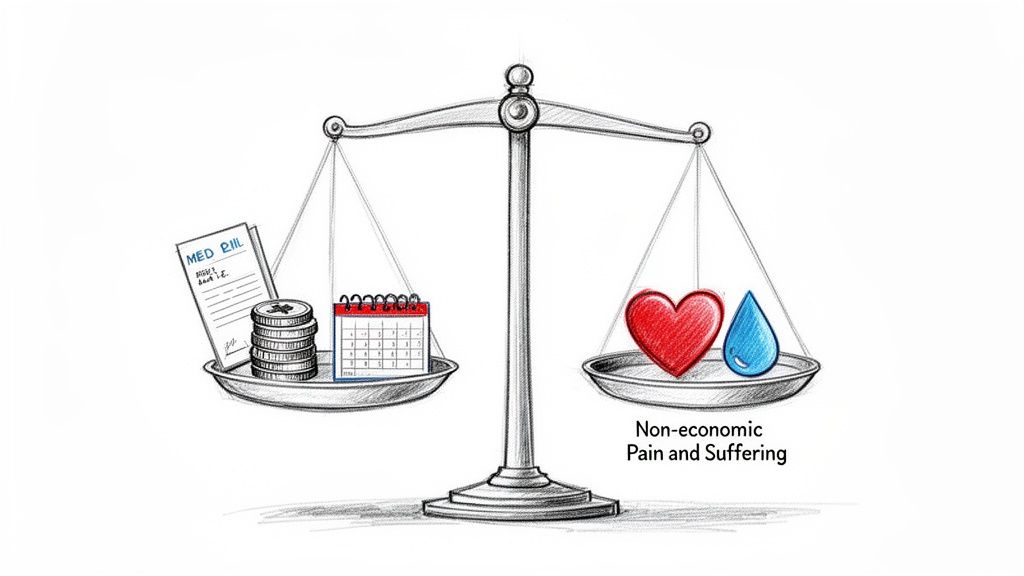

In legal terms, this compensation is called damages. It's not one big, arbitrary number; instead, it's carefully broken down into two different categories that, together, paint a full picture of your losses.

Economic Damages: The Tangible Costs

First up are the most black-and-white losses: economic damages. Think of these as anything you can point to on a receipt, an invoice, or a pay stub. They are the direct, out-of-pocket financial hits you’ve taken because someone else was careless.

These are the foundational costs of your claim and typically include:

- Medical Bills: This is the big one. It covers everything from the ambulance ride and the emergency room visit to follow-up surgeries, physical therapy, prescription drugs, and even an estimate for any medical care you’ll need down the road.

- Lost Income: If you were too hurt to work, you can claim the wages you lost. And if your injuries are serious enough to impact your ability to earn a living long-term, that loss of future earning capacity gets factored in, too.

- Property Damage: This one is pretty simple—it’s the cost to get your car fixed or, if it's totaled, its replacement value. It also covers any other personal items damaged in the wreck.

Non-Economic Damages: The Human Cost

The other side of the coin is non-economic damages. These are trickier to calculate because they compensate you for the intangible, human cost of the accident. There's no bill for pain or a receipt for anxiety, but these losses are just as real and often far more significant than the financial ones.

These are the losses that don't come with a price tag. They compensate for the physical pain, emotional distress, and disruption the accident has caused in your daily life.

This is where the law tries to put a value on things like:

- Pain and Suffering: The real, physical pain you've had to endure because of your injuries.

- Mental Anguish: This covers the emotional fallout—the anxiety, depression, fear, or even PTSD that can follow a traumatic crash.

- Physical Impairment: If the accident left you with a permanent limp, a loss of motion in your shoulder, or other lasting physical limitations, this is the compensation for that.

Because these damages are subjective, they are often where the biggest battles with insurance companies are fought. You can get a much deeper look into the different types of damages in personal injury cases to see how each piece is valued.

To see how this plays out, just imagine two different scenarios. A simple fender-bender that causes a mild whiplash might lead to $5,000 in medical bills and maybe a similar amount for pain and inconvenience. But picture a pedestrian who gets hit and needs knee surgery. They could easily be looking at $50,000 in medical costs, a huge chunk of lost wages, and a much, much higher award for non-economic damages to account for the long, painful recovery and permanent mobility issues. Every single detail matters.

Common Questions About Texas Parking Lot Accidents

Getting into a wreck is stressful enough, but when it happens in a parking lot, a whole new set of questions can pop up. Let's tackle some of the most common ones I hear from clients, so you can feel more in control.

Does It Matter That The Crash Was On Private Property?

Yes, it does, but probably not how you're imagining. It's true that police might not write a full-blown accident report for a fender-bender on private property. But that absolutely does not prevent you from filing a claim.

At the end of the day, the same rules of the road and principles of negligence still apply. The driver who caused the crash is still on the hook for the damage. On top of that, if things like giant potholes or dangerously dim lighting contributed to the accident, the property owner themselves could be liable.

Key Insight: A crash on private property is still governed by Texas civil law. The location doesn't give a negligent driver or a careless property owner a free pass. Your right to get compensated is still very much alive.

What Is The Deadline To File A Lawsuit In Texas?

Texas law sets a firm deadline for filing a personal injury lawsuit, which is called the statute of limitations. For almost every parking lot accident case, you have exactly two years from the date of the crash to get your lawsuit filed with the court.

This isn't a suggestion; it's a hard and fast rule. If you miss that two-year window by even a single day, your case will almost certainly be thrown out, and you'll lose any chance of recovering compensation. It's crucial to get the ball rolling long before that deadline gets close.

Should I Accept The First Settlement Offer From The Insurance Company?

My advice? Almost never. The first offer an insurance adjuster throws out is rarely their best one. Think of it as their opening bid in a negotiation. Their job is to save their company money, which means paying you as little as possible.

They often make these lowball offers right away, hoping you're anxious for a quick check and haven't yet realized the full scope of your injuries or expenses. You might still have physical therapy ahead of you, or discover that "minor" back pain is a much bigger deal than you first thought.

Before you even think about accepting an offer, you need a crystal-clear picture of your total damages. That includes:

- All your medical bills—both past and future.

- Wages you lost because you couldn't work.

- The full cost to get your car fixed or replaced.

- Fair compensation for your pain and suffering.

Taking a quick payday can feel tempting, but rushing this decision could cost you thousands. Make sure you understand what your case is truly worth before you sign anything.

Don't guess what your case is worth. Verdictly gives you access to real Texas motor vehicle verdicts and settlements. You can research cases just like yours to see what they were actually worth. Level the playing field and negotiate from a position of knowledge by visiting https://verdictly.co.

Related Posts

A Texas Guide to Your Hit and Run Auto Accident Claim

Involved in a hit and run auto accident in Texas? This guide walks you through the critical steps, your legal rights, and how to value your claim.