how much is my car accident worth - quick, clear estimate

Understand how much is my car accident worth by reviewing damages, fault, and settlement calculations. Get a clear estimate for your claim and next steps.

If you’re asking, "how much is my car accident worth?", you're not alone. It's the first question on everyone's mind, but the answer isn't a simple one. The final number is entirely unique to your specific losses. We can, however, look at the big picture: in 2022, claims for minor injuries averaged around $26,501, but it's not uncommon for severe accidents to push well into six-figure territory.

What Is Your Car Accident Claim Really Worth?

After the shock of a crash wears off, the financial reality sets in. Everyone wants a quick number, but the truth is, there's no magic calculator that can spit out the value of your case. Your claim's worth is built from the ground up, piece by piece, based on the real-world impact the accident had on your life.

Think of it like building a custom home. The final price depends on the foundation, the square footage, the materials, and all the finishing touches. Your settlement works the same way, constructed from two main "building blocks" called damages.

The Two Core Types of Damages

To really get a handle on your claim's value, you need to understand how your losses are separated into two distinct buckets. Each one is critical to reaching a fair final settlement.

- Economic Damages: These are the hard, verifiable costs—the black-and-white financial losses you can prove with receipts and records. This includes every medical bill, the income you lost from being unable to work, the cost to repair your car, and any other direct expenses.

- Non-Economic Damages: This bucket covers the human cost of the accident. These are the profound losses that don't come with a neat price tag, like physical pain, emotional trauma, anxiety, and the inability to enjoy life the way you used to.

Calculating economic damages is mostly just addition. Non-economic damages, on the other hand, are far more subjective. This is where most of the negotiation—and disagreement—with insurance companies happens, and why a solid understanding is so important.

National Averages Tell a Complicated Story

Looking at national data can give you a bit of perspective, but it’s crucial to take it with a grain of salt. For instance, the average car accident settlement in the U.S. as of 2025 is about $212,325, but the median is a much more modest $25,000.

What does that huge gap tell us? It shows that while most cases settle for smaller amounts, a handful of catastrophic injury cases with multi-million dollar payouts pull the average way, way up. Digging into more personal injury law statistics can help you see these trends more clearly.

Your claim’s value isn't based on an average number you find online. It is a direct reflection of your documented financial losses combined with a justifiable amount for your personal suffering, all considered within the unique context of your accident.

So, while asking "what's my case worth?" is the right starting point, the real work is in a detailed accounting of every loss, big and small. By understanding the core components—your economic and non-economic damages—you’ve got the framework you need to build a strong and fair claim.

The settlement you receive is the result of several interconnected elements, each carrying significant weight. Here’s a quick breakdown of what truly drives the final number.

Key Factors That Define Your Settlement Value

| Factor | How It Impacts Your Claim's Worth |

|---|---|

| Severity of Injuries | More serious injuries mean higher medical bills, longer recovery, and greater pain and suffering, all of which substantially increase the claim's value. |

| Total Economic Losses | This is the foundation of your claim. The higher your documented medical costs, lost wages, and property damage, the higher the starting point for settlement talks. |

| Pain and Suffering | The impact on your quality of life is a major component. Chronic pain, emotional distress, or loss of hobbies directly adds to the non-economic value. |

| Degree of Fault | If you are found partially at fault, your final settlement will likely be reduced by your percentage of responsibility. Clear evidence showing the other driver was 100% at fault is ideal. |

| Insurance Policy Limits | The at-fault driver's insurance policy limits create a ceiling on what the insurer will pay. A claim worth $100,000 is limited if the policy only covers $30,000. |

| Quality of Evidence | Strong, clear evidence—like police reports, photos, witness statements, and detailed medical records—makes it harder for the insurer to dispute your claim. |

Ultimately, a strong case is built on a clear understanding of how these factors work together. The more you can substantiate each of these points, the better positioned you will be during negotiations.

Decoding the Damages in Your Settlement

To figure out what a car accident case is really worth, you first have to understand how a settlement is put together. The best way to think about it is like building a house. Your total claim value is the final structure, and it’s made from different "building blocks" called damages. Each block represents a specific loss you’ve suffered, and they all stack up to form the foundation of your compensation.

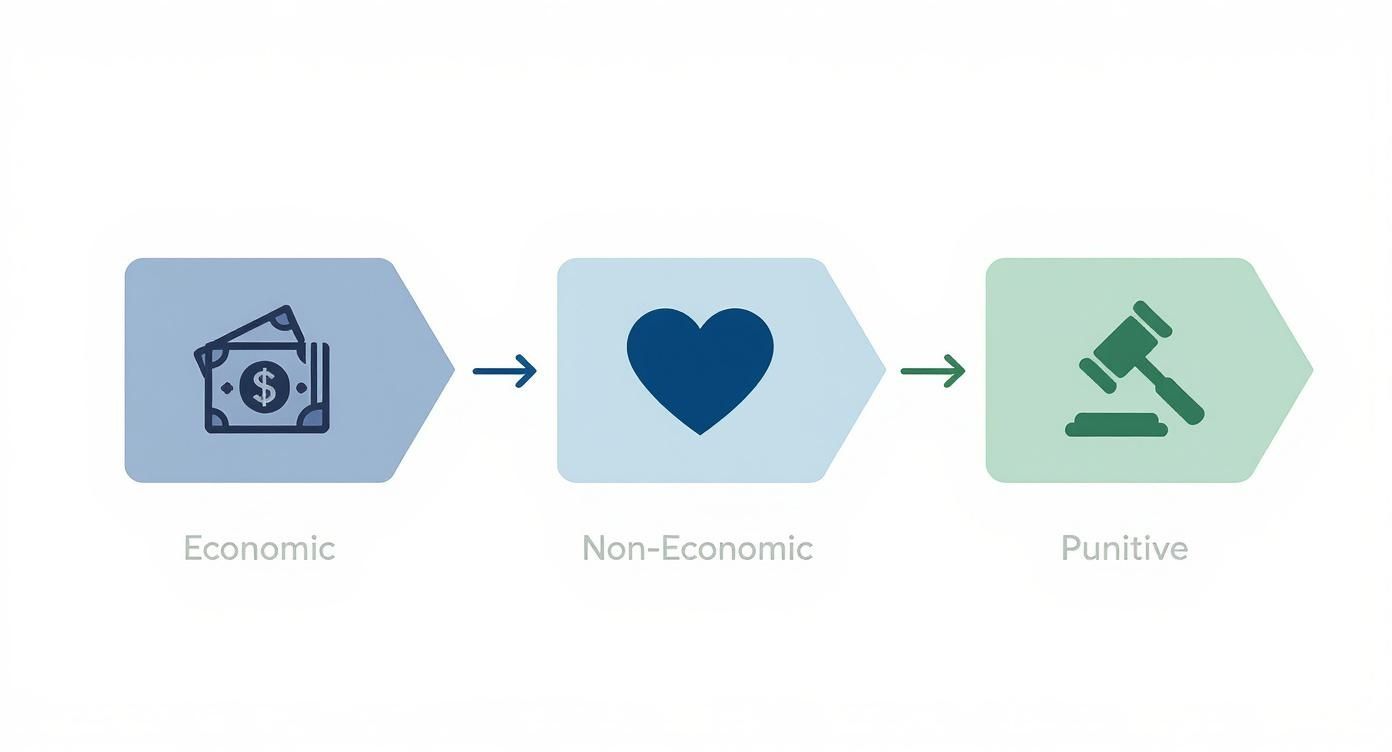

These damages fall into two main categories: economic and non-economic. There's a third type, punitive damages, but honestly, it’s a rare sight in most car accident cases. Let’s break down what each of these really means for you.

Economic Damages: The Receipts of Your Accident

Economic damages are the most clear-cut part of any claim. Why? Because they represent direct, out-of-pocket financial losses that you can prove with a paper trail. These are the tangible costs—the black-and-white numbers backed by bills, receipts, and pay stubs that form the base of your settlement.

Here’s what typically falls under economic damages:

- Medical Expenses: This covers everything from the ambulance ride and ER visit right after the crash to ongoing physical therapy, surgeries, medications, and any medical equipment you might need.

- Future Medical Care: If your injuries are going to require long-term treatment—think future surgeries or years of therapy—the estimated cost for that care is factored in. This is usually established with the help of medical experts who can project those future needs.

- Lost Wages: This one's simple. It’s the income you lost because you couldn't work while recovering. Your pay stubs or a letter from your boss can prove this easily.

- Loss of Earning Capacity: This is different from lost wages. If your injuries permanently limit your ability to do your job or force you into a lower-paying field, this damage compensates for that future loss of income.

- Property Damage: This is the cost to get your car fixed or, if it's totaled, replaced. It also covers any other personal property, like a laptop or phone, that was destroyed in the crash.

When you add all these costs up, the numbers can be staggering. The economic toll of fatal crashes in the US is estimated at $417 billion a year, a figure that includes medical costs, lost productivity, and property damage. For all serious accidents combined, the direct economic costs are around $460 billion. You can dig deeper into these car crash economic impacts to see just how quickly these tangible losses accumulate.

Non-Economic Damages: Valuing the Invaluable

While economic damages cover your wallet, non-economic damages are meant to compensate for the human cost of the accident. These are the deeply personal, intangible losses that don't come with a neat price tag but have a profound impact on your quality of life.

Because these damages are subjective, they are almost always the most contentious part of a settlement negotiation. Proving their value takes more than just receipts; it requires painting a clear picture of your suffering.

Here are the key components of non-economic damages:

- Pain and Suffering: This compensates for the actual physical pain, discomfort, and general misery you have to endure because of your injuries.

- Emotional Distress: This covers the psychological fallout—the anxiety, depression, fear, sleepless nights, or even post-traumatic stress disorder (PTSD) that often follows a traumatic crash.

- Loss of Enjoyment of Life: If your injuries stop you from doing the things you love, whether it's playing with your kids, hiking, or just working in your garden, you can be compensated for that loss.

- Disfigurement: This applies to permanent scars, burns, or other physical changes that alter your appearance.

To prove these kinds of damages, you need to tell your story. Evidence might include a personal journal detailing your daily struggles, photos showing your injuries over time, and even statements from friends and family who can testify to how the accident has changed you. In cases involving life-altering harm, understanding how these damages are calculated is absolutely critical. For a closer look, you can read our detailed guide on settlements for catastrophic injuries.

A Note on Punitive Damages

You’ve probably heard about punitive damages in high-profile cases. Unlike the other damages that are meant to compensate the victim, these are designed to punish the at-fault party for truly reckless or malicious behavior—think of someone driving drunk at 100 mph in a school zone.

It’s important to keep in mind that punitive damages are not a factor in the vast majority of car accident claims. They are reserved for the most extreme cases and are intended to send a message to deter others from similar conduct, not just to cover your losses.

How to Calculate Your Potential Claim Value

Trying to answer "how much is my car accident worth?" often feels like guessing, but there's a method to the madness. While no two cases are identical, insurance adjusters and lawyers typically start with a common formula called the multiplier method. Think of it as a framework for building your claim—a way to connect your real, out-of-pocket costs to the less tangible value of your pain and suffering.

The core idea is pretty straightforward: the more serious and life-altering your injuries are, the higher the multiplier. It’s a way to translate the human experience of an injury into a number that can serve as a solid starting point for settlement talks.

Your total potential settlement is a combination of different types of damages—economic (the bills), non-economic (the human cost), and sometimes punitive (to punish wrongdoing).

This process shows how a claim is built, starting with the concrete financial losses and then adding value to account for how the accident truly affected your life.

Understanding the Multiplier Method

The multiplier method isn't an exact science, but it's a practical and widely accepted way to get the ball rolling. The calculation itself is simple: you add up all your economic damages—things like medical bills and lost income—and multiply that total by a number, usually somewhere between 1.5 and 5.

So, what determines if you're closer to a 1.5 or a 5? It comes down to a few critical factors:

- Severity of the Injury: A minor sprain that heals quickly might land a 1.5x multiplier. A serious injury needing surgery and long-term care could easily justify a 4x or 5x multiplier.

- Length of Recovery: The longer and more difficult your road to recovery, the stronger the case for a higher number.

- Impact on Daily Life: Were you unable to work, enjoy your hobbies, or take care of your family? The more your life was disrupted, the higher the multiplier.

- Permanent Impairment: Any lasting issues, like chronic pain, scarring, or limited mobility, will significantly push the multiplier up.

The multiplier method provides a baseline for negotiation. It’s a tool to begin the conversation, not a final, legally binding calculation. An insurer will almost always argue for a lower multiplier, while your attorney will present evidence to justify a higher one.

Let's look at a couple of real-world scenarios to see how this plays out.

Example Settlement Calculations

To illustrate how this works, let's compare two very different injury cases. One is a fairly minor, straightforward injury, while the other is a life-changing event. The table below shows how the exact same formula can lead to vastly different outcomes based on the severity of the accident.

| Damage Component | Example 1: Minor Injury (Whiplash) | Example 2: Severe Injury (Herniated Disc) |

|---|---|---|

| Total Medical Bills | $3,500 | $60,000 |

| Lost Wages | $1,500 | $15,000 |

| Total Economic Damages | $5,000 | $75,000 |

| Multiplier Applied | x 2 (for a minor, temporary injury) | x 4 (for a severe, permanent injury) |

| Non-Economic Damages | $10,000 | $300,000 |

| Estimated Total Settlement | $15,000 | $375,000 |

As you can see, the severity of the injury and its ongoing consequences dramatically increase both the multiplier and the final settlement value. These examples show why it’s so critical to document not just your bills, but the entire story of your recovery.

To get a better handle on the back-and-forth of negotiations, you can dive deeper with our complete guide to car accident settlements.

Factors That Can Reduce Your Final Payout

Coming up with a number for your damages is a great start, but it's rarely the end of the story. The initial calculation is just a starting point, and several real-world factors can shrink that figure before you ever see a check.

Two of the biggest hurdles you’ll likely face are comparative fault and insurance policy limits. Think of them as potential roadblocks that can either reduce your compensation or put a hard ceiling on what you can actually recover, no matter how high your medical bills are. Let's break down how they work.

How Your Role in the Accident Matters

It would be simple if every crash had one driver who was 100% at fault and another who was a complete victim. But reality is often messier. Insurance adjusters will pick apart every detail of the accident to see if they can pin some of the blame on you—even if the other driver was clearly the main cause. This is a legal concept called comparative fault.

Imagine it like a pie chart of responsibility. If a jury decides you were 20% at fault—maybe you were going a few miles over the speed limit when someone else blew through a stop sign—your final award gets cut by that exact percentage.

A $100,000 award would shrink to $80,000 if you're found 20% at fault. The more blame they can assign to you, the less money you walk away with.

How this plays out depends on your state. Texas, for instance, follows a "modified comparative fault" rule. This means you can collect damages as long as you aren't found to be more than 50% responsible. The moment your share of the blame hits 51%, you get nothing. Zero. This is why fighting over every percentage point of fault is so critical, especially in tricky situations like a single-car accident where fault is not immediately clear.

The Hard Cap of Insurance Policy Limits

The other major factor that can limit your payout is the at-fault driver's insurance coverage. Every auto policy has a policy limit, which is the absolute maximum amount the insurance company will pay out for a single claim. It doesn't matter if your damages are five times that amount; the insurer's legal obligation stops at the policy limit.

Let's say your medical bills, lost wages, and other damages total $150,000. If the driver who hit you only has the state minimum liability coverage of $30,000, their insurance company is only on the hook for that $30,000. You’re left with a $120,000 gap that their insurer simply will not pay.

This is where your own insurance policy becomes a critical safety net. There are two types of coverage designed for this exact situation:

- Uninsured Motorist (UM) Coverage: This covers your losses if you're hit by a driver with no insurance at all.

- Underinsured Motorist (UIM) Coverage: This kicks in when the other driver has insurance, but their policy limits aren't high enough to cover all your bills.

Without UM/UIM coverage, your only remaining option is to sue the at-fault driver personally. The hard truth is that most drivers carrying minimum insurance don't have the personal assets to satisfy a large court judgment. This makes actually collecting the money you're owed incredibly difficult. Checking your own policy now to make sure you have solid UM/UIM protection is one of the smartest financial decisions you can make.

Gathering Evidence to Maximize Your Claim

Figuring out what your claim is worth is only half the battle. The other, arguably more important half, is proving it with rock-solid evidence. Think of it this way: strong, organized documentation is the engine that drives a successful claim. Without it, even the most legitimate case can sputter out.

An insurance adjuster's job is to scrutinize every detail. They aren't going to take your word for anything. Every single dollar you ask for, whether it's for a physical therapy bill or a lost day of work, has to be backed up by a piece of paper. This is your chance to build an airtight case that leaves no room for doubt and puts you in the best position for a fair settlement.

Medical Records That Tell Your Whole Story

Your medical file is the absolute cornerstone of your claim. It’s what backs up both your tangible bills and your intangible suffering. Just having a single bill from the emergency room won't cut it. You need to create a complete, chronological record that shows the full scope of your injuries and your entire recovery journey.

The goal is to paint a crystal-clear picture of your medical reality. Your file should include:

- Initial Treatment Records: This means the ambulance report, ER intake and discharge papers, and notes from your very first follow-up appointments.

- Ongoing Care Documentation: Collect every record from specialists, physical therapists, chiropractors, and surgeons you visit. Each appointment adds another layer of proof.

- Diagnostic Test Results: Make sure you have copies of all MRIs, X-rays, CT scans, and any other imaging that confirms what you're dealing with.

- Prescription Receipts: Keep copies of every prescription you get filled for your accident-related injuries. This demonstrates an ongoing need for medical care.

This paper trail does more than just add up your medical bills; it provides the essential foundation for calculating your pain and suffering.

Proving Your Financial Losses

Beyond the doctor's office, your claim needs to account for every dollar the accident has cost you in lost wages and other out-of-pocket expenses. Just saying you missed work isn't enough—you have to prove it. This is where your financial records become absolutely indispensable.

To build a compelling case for your economic damages, you'll need to pull together:

- Pay Stubs: Gather pay stubs from before and after the accident. This creates a simple, undeniable before-and-after snapshot of your earnings.

- Employer Letter: A formal letter from your boss confirming your job title, pay rate, and the specific dates you couldn't work because of your injuries is incredibly powerful.

- Tax Returns: Your past tax returns can help establish your average annual income. This is crucial if you need to argue for a loss of future earning capacity.

This documentation turns your claim from a simple estimate into a verifiable financial statement. It’s also wise to consider the future. Trends show that compensation for care is on the rise due to wage inflation for medical professionals. This means valuations for future care are increasingly reflecting these economic shifts, a factor that can significantly impact your claim's final value. You can read more about how caregiver wage data impacts injury claims.

Key Takeaway: Every receipt, bill, and pay stub is a piece of the puzzle. The more complete your financial picture, the stronger your negotiating position will be with the insurance company.

Documenting Your Pain and Suffering

Finally, you have to find a way to show the human cost of the accident—your non-economic damages. This is often the trickiest part of a claim because it's so subjective, which makes compelling documentation absolutely essential. You have to show, not just tell, how this accident has upended your life.

Here are some of the most effective ways to document your suffering:

- Start a Personal Injury Journal: Write in it every day. Detail your pain levels, physical struggles, emotional state, and any family events or hobbies you had to miss. This creates a powerful, real-time narrative of your experience.

- Take Photographs and Videos: Document your injuries as they heal. Pictures of bruises, casts, or surgical scars provide visceral proof of your trauma. A short video showing how you now struggle with a simple task like opening a jar can be even more impactful.

- Get Statements from Loved Ones: Ask friends, family, or even coworkers to write a few sentences about the changes they’ve seen in you since the crash. Their outside perspective provides crucial third-party validation of your suffering.

This kind of evidence helps an adjuster or jury see that your losses go far beyond what can be tallied on a calculator. It gives a voice to your pain and makes a much stronger case for a higher settlement.

Answering Your Top Questions About Claim Value

Once you get a handle on the different types of damages, the role of fault, and the importance of evidence, you’re still left with some big, practical questions. The road from the accident to a final settlement can feel like a maze. Let’s clear up some of the most common questions that pop up, so you know what to expect.

Knowing what’s coming can make a world of difference. It puts you back in the driver's seat, ready to make smart decisions as you navigate your claim.

How Long Will My Car Accident Settlement Take?

This is the million-dollar question, and the honest answer is: it really depends on your specific case. A straightforward claim with minor injuries and zero dispute over who was at fault might wrap up in a few months. It's just a matter of adding up the bills and coming to a fair number for the hassle.

But when things get more complicated, a case can easily stretch out for a year or even longer, especially if you have to file a lawsuit. One of the biggest holdups is reaching what’s called Maximum Medical Improvement (MMI). This is the point where your doctor says your condition is as good as it’s going to get, and they have a clear picture of what your future medical care looks like.

Most good attorneys will tell you to pump the brakes on settling before you hit MMI. Why? If you take an offer too soon, you’re gambling with your future. You could be leaving a huge amount of money on the table that you'll desperately need for treatments down the line. Rushing almost always means getting a lowball payout that doesn't cover your actual long-term costs.

Should I Take the First Offer from the Insurance Company?

In almost every single case, the answer to this is a hard "no." Think of the insurance company’s first offer for what it is: the opening bid in a negotiation, and a low one at that. Adjusters are trained professionals, and their job is to protect their company's bottom line by closing your claim for as little money as possible. That first offer is a test to see if you'll bite on a quick, cheap payout before you even know the full financial damage from your injuries.

The first offer almost never accounts for the full scope of your future medical needs, your total lost earning potential, or the true value of your pain and suffering.

Once you accept it, that's it—you sign away your rights to ever ask for more money for this accident. Always treat that first offer as the start of a conversation, and never, ever sign anything until an experienced attorney has looked it over and can tell you what your car accident is actually worth.

Do I Need a Lawyer to Determine My Claim Worth?

While a guide like this can give you a solid footing, it’s no substitute for advice tailored to you. Only an experienced personal injury lawyer can give you a truly accurate valuation based on the unique details of your accident, the specific laws in your state, and what juries and insurers have paid out in similar local cases.

A lawyer brings a few critical things to the table:

- Knowing the Evidence: They know exactly what documents and proof you need to build a rock-solid case and how to get it.

- Expert Connections: They can bring in medical and financial experts to professionally map out your future costs and lost income.

- Negotiation Muscle: They deal with insurance adjusters every single day. They know the tactics, they know the pressure points, and they know how to push back effectively.

The numbers don’t lie: people who hire a lawyer consistently get much higher settlements—often several times more—than those who go it alone. And since most personal injury attorneys work on a contingency fee basis, you don’t owe them a dime unless they win or settle your case.

Is It Likely My Car Accident Case Will Go to Trial?

It's highly unlikely. The overwhelming majority of personal injury cases—somewhere around 95%—settle out of court. A trial is a long, expensive, and stressful gamble for everyone, including the insurance company. Because of that, both sides are heavily motivated to find a fair middle ground through negotiation.

Filing a lawsuit is usually a strategic move, a last resort when the insurance company flat-out refuses to offer a reasonable amount. A great attorney prepares every case as if it's headed for a courtroom, because that show of strength is often what brings the insurer to the negotiating table with a much better offer. The goal is always to get you a just settlement without you ever having to see the inside of a courtroom.

Understanding the true value of your case starts with having the right data. Verdictly gives you access to real Texas verdicts and settlements, so you can see what cases like yours are actually worth and walk into negotiations with confidence. Explore our database today at Verdictly to get the insights you need.

Related Posts

How Much Can I Get From a Car Accident Settlement?

Wondering how much can I get from a car accident? This guide breaks down settlement factors, damages, and claim values to help you estimate your compensation.

Using a Compensation Calculator for Car Accident Claims

Discover how to use a compensation calculator for car accident claims in Texas. Get practical steps for estimating your settlement value with real-world data.

A Guide to Medical Records Reviews in Personal Injury Claims

Learn how medical records reviews can strengthen your Texas injury claim. This guide explains the process, key findings, and how to build a stronger case.