Using a Bodily Injury Calculator to Value Your Claim

Learn how a bodily injury calculator can estimate your settlement. Our guide covers economic damages, pain and suffering, and key claim adjustment factors.

Wondering what a bodily injury calculator can do for you? Think of it as a starting point. It's great for adding up hard numbers like medical bills and lost wages to get a baseline estimate of your personal injury claim.

But that's all it is—a starting point. It simply cannot accurately value your unique pain and suffering or navigate the complex legal factors that will shape your final settlement.

What a Bodily Injury Calculator Actually Tells You

Before you start punching in numbers, let’s be clear about what these calculators are really for. It’s less of a crystal ball predicting a guaranteed payout and more of a powerful organizational tool. Its main job is to help you get a handle on the tangible, black-and-white costs of your injury.

These tools are fantastic for creating that foundational estimate. They force you to gather all your concrete financial losses in one place, making sure nothing falls through the cracks. This step is essential for building the initial, evidence-based part of your claim.

Setting Realistic Expectations

The single biggest mistake I see people make is treating a calculator's output as the final word. The number it spits out is just a mechanical sum of your inputs. It’s a necessary piece of the puzzle, but it’s far from the whole picture.

A simple calculator just can't see the full story. For instance, it can't:

- Grasp the Emotional Toll: There’s no field to enter the anxiety, sleepless nights, or trauma that comes after a serious accident.

- Understand Personal Suffering: A broken leg is a massive career-altering event for a construction worker, but it's different for someone with a desk job. The calculator doesn't know your life or your story.

- Factor in Legal Nuances: It has no idea about the specific laws in your state, the reputation of the insurance adjuster you're up against, or the defendant’s policy limits.

The number you get is an informational first step—a way to organize your thoughts, not a figure to take to the negotiating table. Its real value is in helping you frame a more productive conversation with a qualified attorney who can interpret all those critical nuances.

An online calculator tells you the what—the sum of your measurable losses. A legal professional tells you the why—why your specific circumstances, suffering, and local laws justify a certain settlement range.

The Bigger Financial Picture

Understanding your claim's potential value means seeing where you fit into a much larger system. Consider this: the global accident insurance market, which covers bodily injuries, was valued at around $90.01 billion in 2025 and is projected to skyrocket to $159.60 billion by 2034.

This massive financial scale is exactly why insurance companies scrutinize every single detail of a claim. You can dig into more data on the accident insurance market and its growth to see what you're up against. Your calculated estimate is simply your entry ticket into this incredibly complex financial arena.

Tallying Your Economic Damages for a Solid Foundation

This is where the rubber meets the road. Before you can even begin to think about concepts like pain and suffering, you have to build a rock-solid, evidence-backed total of your economic damages. These are the concrete, provable financial losses you’ve suffered as a direct result of your injury.

Think of this part of your claim as its undeniable foundation. Every single dollar must be accounted for with a corresponding document—a bill, a receipt, a pay stub. Getting this right is your most powerful tool in the early stages of a claim.

Calculating Every Medical Expense

Start by gathering every single medical bill connected to the accident. This goes way beyond just the big hospital invoice. It includes every single touchpoint you've had in your recovery journey.

You can't afford to leave anything out. Your list of medical expenses should include:

- Emergency Services: That ambulance ride, the ER visit, and any immediate treatments you received.

- Hospital Stays: All costs tied to inpatient care, from the room charges to surgeries and specialist consultations.

- Ongoing Treatments: Don't forget physical therapy, chiropractic adjustments, follow-up appointments, and prescriptions.

- Medical Equipment: Tally the costs for crutches, braces, or any other durable medical equipment your doctor prescribed.

It's crucial to keep a dedicated folder, whether digital or physical, for these documents. Supreme organization here forms the baseline for any bodily injury calculation. It’s also worth noting that even smaller jury awards, like an Austin jury's verdict in a rear-end collision case, are built on this kind of meticulous proof.

Looking ahead is just as important. Talk to your doctor about your long-term prognosis. You’ll need a professional opinion on potential future surgeries, ongoing therapies, or long-term medication needs. This documentation is vital for calculating future expenses.

A shoebox full of crumpled receipts just won't cut it. Create a simple spreadsheet listing the provider, date of service, and cost for every expense. This organized list becomes your summary of damages—an incredibly powerful document for you and your attorney.

Accounting for Lost Income and Earning Capacity

Next up is calculating every dollar of lost income. This isn't just about your base salary; it's the total compensation you would have earned had the injury never happened. Grab your pay stubs from before the accident to establish a clear, provable baseline of your average earnings.

Your calculation should include:

- Wages and Salary: The direct income you lost while unable to work.

- Lost Overtime: If you consistently worked overtime, calculate the average you missed out on.

- Missed Bonuses & Commissions: Document any performance-based pay you were unable to earn.

If your injuries are severe enough to affect your long-term career path, you might also have a claim for lost earning capacity. This calculates the difference between what you would have earned over your lifetime and what you can now realistically earn. Proving this often requires input from vocational and economic experts, but it's a critical component for serious injuries.

To give you a sense of scale, workplace injuries alone cost the U.S. economy $167 billion in 2022. Businesses spend over $1 billion each week on these related losses. These staggering figures highlight why accurately tallying every penny of your personal economic damages is so critical for a fair outcome.

Putting a Price on Pain and Suffering

This is where things get tricky. Calculating the value of your pain and suffering—what the insurance world calls "non-economic damages"—is the most subjective part of any injury claim. There's no bill or receipt for physical pain, emotional anguish, or the life you couldn't live while you were recovering.

Unlike your medical bills and lost wages, this part of the calculation requires a human touch. It’s about turning your very real, but intangible, hardship into a number that the other side will accept. This is where experienced adjusters and attorneys earn their keep, but you can understand the methods they use.

The two go-to methods for this are the Multiplier Method and the Per Diem Method. Let's break down how they work.

The Multiplier Method Explained

The Multiplier Method is the one you’ll see most often. The concept is simple: take your total hard costs (medical bills + lost wages) and multiply them by a specific number, usually somewhere between 1.5 and 5.

That number—the "multiplier"—is everything.

So, where does it come from? It’s not random. The multiplier is a reflection of how severe your injuries are and how much they’ve impacted your life. A minor sprain that heals up in a month with a few doctor visits might only justify a 1.5 multiplier. On the other hand, a serious injury with permanent consequences could easily command a 4 or 5.

Let’s look at a couple of real-world examples:

- Scenario A: The Broken Arm. Someone breaks their arm in a fall. They’re in a cast for six weeks, miss a little work, and get back to normal after some physical therapy. Their multiplier is probably going to land in the 2 to 2.5 range.

- Scenario B: The Chronic Back Injury. A car accident leaves another person with a herniated disc. They're now dealing with chronic pain, facing long-term treatment, and can't go back to their old job. This is a life-altering injury, so their multiplier could easily be a 4 or even higher.

The difference is clear. It all comes down to the duration of the pain, the permanence of the injury, and the overall hit to that person's quality of life.

The Per Diem Approach

Another way to look at it is the Per Diem Method. "Per diem" just means "per day." With this approach, you assign a daily dollar amount to your suffering for every day from the accident until your doctor says you've reached "maximum medical improvement."

What’s a fair daily rate? A common starting point is your daily wage. The logic is that dealing with the pain and disruption of an injury is at least as demanding as going to work each day.

If you earn $200 a day and your recovery takes 100 days, the pain and suffering calculation would be $20,000 ($200 x 100). This method works best for short-term injuries where there's a clear end date to your recovery.

Ultimately, picking a method is less about the formula and more about telling a convincing story. The evidence you gather—your medical records, a personal journal detailing your struggles, even statements from family and friends—is what will justify the number you’re asking for.

Keep in mind that where you live matters. A lot. Bodily injury values can vary wildly from one state to another, or even one county to the next, because of local laws and jury tendencies. It's such a big factor that global organizations like The Lloyd's Market Association now use an International Bodily Injury Index to track these differences. You can see for yourself how global bodily injury awards are benchmarked and why getting a local perspective is so critical.

Adjusting Your Estimate with Real-World Factors

So, you’ve run the numbers through a bodily injury calculator and have an initial figure. That's a great starting point, but I have to be honest with you—it’s just a raw number. It doesn't account for the messy, complicated realities of the legal and insurance worlds.

Two huge factors can dramatically change what you actually walk away with: comparative fault and insurance policy limits. Getting a handle on these concepts is what separates a theoretical claim value from the actual check you might receive.

How Your Share of the Blame Reduces Your Payout

Rarely is an accident 100% one person's fault. In the real world, courts and insurance adjusters often find that both parties share some of the blame. This is where the legal concept of comparative fault (sometimes called comparative negligence) comes into play, and it has a direct impact on your wallet.

Here’s how it works: your final settlement is reduced by whatever percentage of fault is assigned to you. For instance, let's say another driver blew through a red light and T-boned you, but you were going a few miles over the speed limit. An adjuster might assign you 20% of the fault for the crash.

This isn't just a minor detail. If your total damages add up to $50,000, that 20% fault finding will slash your potential recovery by $10,000. The most you could get in that case is $40,000. The more blame they can pin on you, the less they have to pay.

Impact of Fault on Settlement Value

This table gives you a clear picture of how different fault percentages can shrink your settlement.

| Initial Claim Value | Your Percentage of Fault | Adjusted Settlement Amount |

|---|---|---|

| $75,000 | 10% | $67,500 |

| $75,000 | 25% | $56,250 |

| $75,000 | 50% | $37,500 |

As you can see, the financial hit adds up quickly.

It's also critical to know your state’s rules. Many states, like Texas, use a "modified comparative fault" system. Under this rule, if you're found to be 51% or more responsible for the accident, you can’t recover a single dime. You get nothing.

The Hard Reality of Insurance Policy Limits

This next part is a tough pill to swallow for a lot of people I've worked with. No matter how high your medical bills climb or how severe your pain and suffering is, you can’t get more money than the at-fault driver's insurance policy covers. These are called policy limits.

Let's walk through a common scenario. You’ve meticulously calculated your damages, and they come out to $100,000. It's a solid, well-documented claim. The problem? The driver who hit you only carried the state minimum liability coverage, which might be just $25,000 for bodily injury.

In this situation, the at-fault driver's insurance company is only on the hook for up to their policyholder's limit. Even with a valid $100,000 claim, the absolute most they are legally required to pay you is $25,000.

This is why understanding policy limits from the get-go is essential for setting realistic expectations. While you might have other options—like tapping into your own Underinsured Motorist (UIM) coverage—the at-fault party's policy limit is the first and most significant ceiling on your recovery. We dive much deeper into navigating these issues in our complete guide to car accident settlements.

Let's Walk Through a Real-World Claim

Theory is one thing, but let's see how this all plays out in a real-world scenario. We'll follow the case of a fictional client, Maria, a marketing manager who got hurt when another driver blew through a red light. Her story is a perfect example of how an initial estimate gets whittled down by the realities of the insurance process.

First things first, we need to add up all of Maria's concrete, provable losses. These are her economic damages, and they form the undisputed foundation of her claim.

- Medical Bills: The ER visit, surgery for her broken tibia, and all the follow-up appointments with the orthopedist came to $28,500.

- Physical Therapy: Her recovery involved a tough six-month rehabilitation program, adding another $6,000.

- Lost Wages: Maria couldn't work for eight weeks. Between her salary and a performance bonus she missed out on, her lost income totaled $12,500.

So, right off the bat, her hard costs—the economic damages—are $47,000. This number is our non-negotiable starting point.

Putting a Number on Pain and Suffering

Now for the tricky part: quantifying the impact on Maria’s life. This wasn't just a minor injury. It required surgery and a long, painful recovery that completely sidelined her from the active lifestyle she loved. Given the severity, the long recovery time, and the significant disruption to her life, a multiplier of 3 feels right for the case.

Applying that multiplier is simple math: $47,000 x 3 = $141,000 for her non-economic damages.

When we put it all together, we get a total initial claim value: $47,000 (Economic) + $141,000 (Non-Economic) = $188,000. This figure represents the full, pre-adjustment value of her claim. To get a feel for how this compares to actual outcomes, it's always smart to look at what juries have awarded in similar cases. You can see real-world examples by checking out jury awards for motor vehicle accident injuries.

Where Reality Kicks In: Adjustments and Reductions

Here's where the negotiation—and the complications—truly begin. The at-fault driver's insurance adjuster digs in and claims Maria was driving 5 mph over the speed limit. Based on this, they argue she shares 10% of the fault for the crash. This is a classic insurance company tactic.

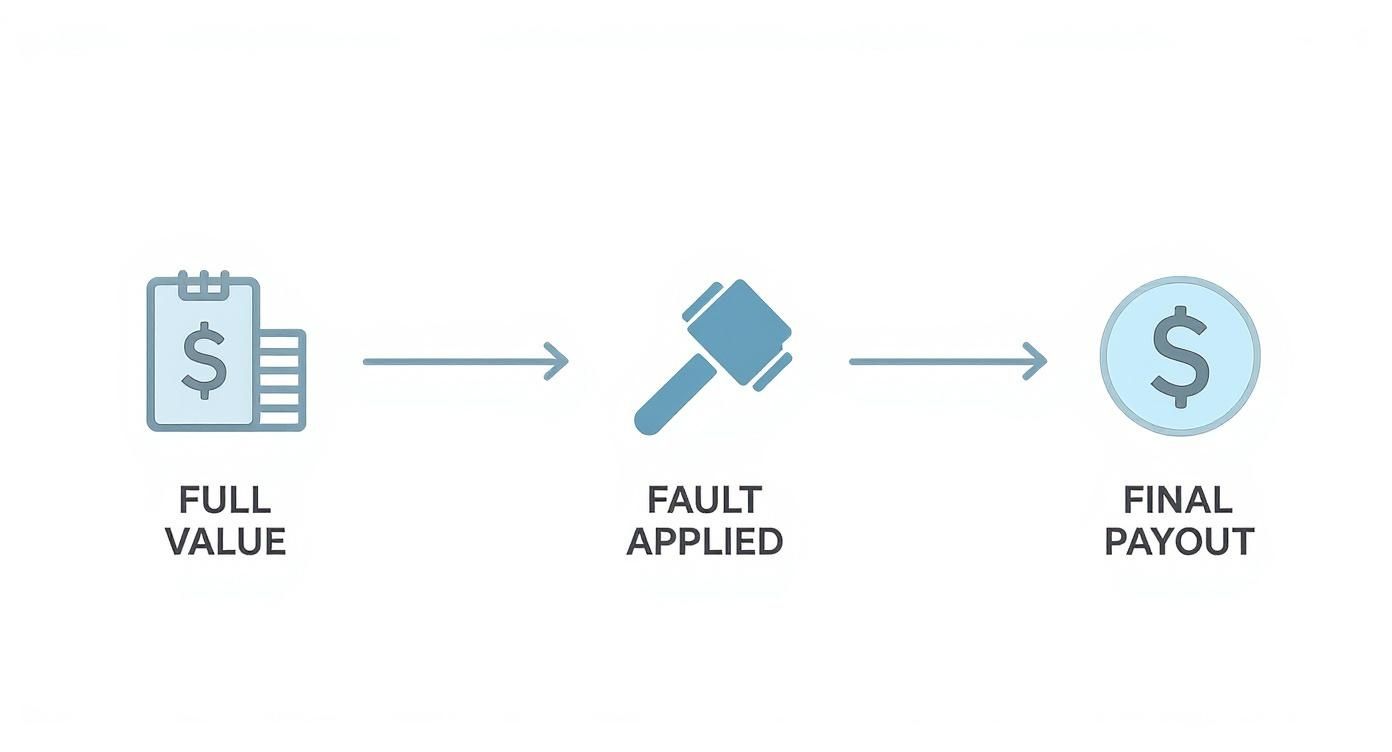

The concept of shared fault is a game-changer. That initial claim value is never a guarantee. It's just the opening bid in a negotiation where things like comparative fault and insurance policy limits will inevitably chip away at the final payout.

This infographic breaks down exactly how a settlement's full value gets reduced once fault is factored in.

It’s a clear visual reminder that even with a solid case, outside factors can take a direct cut from what you ultimately recover.

If we accept their 10% fault argument, it immediately reduces her claim value by $18,800 ($188,000 x 0.10). Suddenly, her adjusted claim value drops to $169,200.

But then comes the biggest wall of all: the at-fault driver's insurance policy. We discover it has a bodily injury liability limit of just $100,000. It doesn't matter that Maria's adjusted claim is worth $169,200. The absolute most the insurance company is legally required to pay is their policy limit.

This leaves Maria looking at a potential settlement of $100,000. It’s a harsh lesson that shows the massive gap between a calculator's theoretical estimate and the hard limits of the insurance system.

Frequently Asked Questions

It's natural to have questions when you're trying to figure out what your injury claim might be worth. A calculator is a fantastic starting point, but knowing its limits is just as important as knowing how to use it. Let's walk through some of the most common questions that come up.

What Is a Fair Multiplier for Pain and Suffering?

This is the million-dollar question, and the honest answer is: it completely depends on your specific case. There’s no magic number. The multiplier is really just a way to translate your personal story into a figure, and that story has to be backed by solid evidence.

As a general rule of thumb, here’s what I’ve seen in my experience:

- For minor injuries—think sprains or strains where you recover pretty quickly—a 1.5x to 2x multiplier is a common starting point.

- When you're dealing with something more serious, like a broken bone or a herniated disc that needs more than just a few doctor's visits, you're often looking in the 3x to 4x multiplier range.

- A 5x multiplier or even higher is typically reserved for catastrophic injuries that change your life forever—things like traumatic brain injuries, paralysis, or significant scarring.

The goal isn't just to pick a number, but to justify it with medical records, photos, and a clear narrative of how the injury has truly affected your day-to-day life.

Can I Trust an Online Bodily Injury Calculator?

Think of an online calculator as an educational tool, not a crystal ball. It’s excellent for getting a ballpark figure based on the hard numbers you plug in, and that alone is incredibly valuable for understanding the basic math of your claim.

But a calculator has blind spots. It doesn't know the specifics of local laws, the negotiation style of the adjuster you're up against, or the defendant's policy limits. It’s a great first step, but it's no substitute for a detailed conversation with a legal pro who understands the full context.

How Do I Calculate Lost Wages If I Am Self-Employed?

This is where documentation is your best friend. Proving lost income when you don't have a regular W-2 requires you to paint a clear financial picture of what you were earning before the accident and what you lost because of it.

You'll need to gather everything you can, such as:

- Past tax returns to show a consistent earning history.

- Profit and loss statements that demonstrate a noticeable dip in revenue right after you were injured.

- Invoices, canceled contracts, or records of appointments you couldn't keep.

- Letters or emails from clients confirming that you had to turn down work because of your injuries.

Should I Share My Calculator Estimate with the Insurance Adjuster?

I would strongly advise against it. Your calculator estimate is a tool for your own preparation—it's part of your private homework.

Sharing that number with an adjuster can lock you into a figure too early in the process, before the full story of your claim has been told. You're essentially showing your cards before the game has even started.

Instead, lead with your documented hard costs (medical bills, lost wages) and a powerful, human account of your pain and suffering. Let your attorney take all that evidence and strategically negotiate the final settlement number.

Gain the informational advantage before you negotiate. With Verdictly, you can see what real cases like yours are worth in Texas, based on actual jury verdicts and settlements. Stop guessing and start knowing. Explore real case values on verdictly.co.